What to Know B-4 Filling out a W-4

When I got my first job at sixteen my new boss handed me a form that asked me how many allowances I wanted to take. “Allowances?! Mom told me in no uncertain terms I had to take this job because I WASN’T getting an allowance anymore.”

So just what was this allowance thing anyway? Essentially, withholding allowances are different life circumstances that directly affect how much money is withheld from your pay. (i.e. Are you single or married? Can anyone else claim you as a dependent? Do you have children or dependents? Do you work more than one job? etc.)

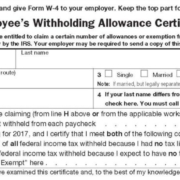

I give you the mystical, magical, famous Form W-4 (*tada*). The IRS requires new employees to fill this out for their employers….looks like this (click to enlarge):

This worksheet is to help your employer know how much to withhold from your paycheck. The top part of page one, as well as page two, are for your use only. These parts are to help you figure out how many allowances you are entitled to take. Page two gets into more specifics for example, if you and your spouse both work, you’re single and work more than one job, or if you plan to itemize.

So what’s it all mean?

More allowances…Mo’ Money

The more allowances you claim, the less income tax will be withheld from your paycheck- aka mo’ money. However, this mean, yes you get more money in your paycheck and less tax taken out in that moment, but in the future this could mean you’ll owe the IRS mo’ money, which could translate to mo’ problems…depending on how you feel about making a payment to the IRS.

Less allowances…Mo’ Refund

The alternative to this is you claim less allowances, so taking more tax from your paycheck up front, meaning in the short term your paycheck will be a little less, but come April, you are more likely to get a refund from the IRS than owe them money.

An additional option…Withhold Additional Money

You can also choose to have additional money withheld from each paycheck if you’d rather pay the IRS upfront and not chance owning come April (this is where a conversation with your CPA could be helpful…have them do an estimate to ensure you’re withholding the correct amount).

Bottom line- The total number of allowances you claim impacts the size of your paycheck and whether you will get a refund or owe money come April.

The key to this, as in anything in life really, is finding balance and what works for you. Would you rather have a little less in your paycheck now and not owe much or maybe even anything in April? Or do you prefer to have more of your money now and plan on paying later? As always, if you’re unsure about how something may affect you financially, you should reach out to your friendly CPA to have the conversation about what may be best for your given situation.

We are pleased to announce that our own Jillian Smith has won the 2016 Practitioner Excellence Awards- Millennial Award this year!

We are pleased to announce that our own Jillian Smith has won the 2016 Practitioner Excellence Awards- Millennial Award this year!